It's been a nice -- and welcome -- bull run of late for shares of Guess? (GES), which have rallied better than 25 percent since fourth quarter earnings and weak guidance for fiscal 2014 (ending January) sent the stock tumbling toward $25 per share. The rally culminated with an 8.3 percent gain last Friday, after the release of first quarter results after the bell Thursday, which briefly pushed the stock to a 52-week high:

GES data by YCharts

The problem for Guess? is that the rally simply made no sense. As I noted in March, the FY13 results and FY14 outlook showed a company with serious, structural issues, a host of macro headwinds, most notably in Europe, and no simple way out of the morass. And, despite the post-earnings bounce, last week, Q1 results weren't any better. The trading response to the quarter was summed up by CNBC's Jim Cramer, who argued, "It's horrendous to me, but it wasn't horrendous enough, so the stock goes higher."

Indeed, it was not a good quarter. Earnings per share did come in ahead of company guidance, but year-over-year fell by more than half, even excluding charges related to restructuring efforts aimed at creating cost savings. Revenue fell 5 percent from the year-prior quarter; North American same-store sales fell 9 percent; comps fell "in the high-single digits" in Europe, according to CFO Nigel Kershaw on the Q1 conference call. Perhaps most notably, the company maintained its full-year earnings guidance, as the impact of higher-than-expected EPS in Q1 is expected to be negated by weaker-than-expected revenue in Europe and Asia.

In fact, revenue guidance for FY14 was actually pulled down slightly, with same-store sales expected to fall in the "mid-single-digits" according to North American Retail CFO Russell Bowers on the earnings call, and total revenues to decrease year-over-year as well.

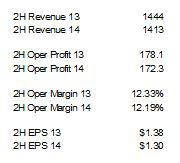

It's als! o far from clear that Guess? will hit its full-year earnings target (it's worth noting that the company pulled down its guidance after last year's second quarter, and only barely hit the bottom of end of the revised range by year's end). At the midpoint of its second quarter guidance, Guess? is guiding for a second half that almost mirrors its second half a year ago:

data from author calculations, using midpoint of full-year fiscal 2014 and second quarter fiscal 2014 guidance

Bear in mind that in fiscal 2013, Guess? saw North America Retail same-store sales drop 6.6 percent, and comps in Europe drop "in the high single-digits" (according to the company's 10-K). Company-wide operating margin fell 450 basis points year-over-year, total revenues declined from fiscal 2012, and net earnings fell by one-third. Now, after a weak first quarter and a second quarter that is guided for another revenue decline (and a 26 percent fall in earnings per share), the company is projecting that it will have largely stemmed the bleeding by the second half of this year.

Perhaps it will. But even so, at its current valuation, that hardly justifies the stock price. At the midpoint of FY14 guidance, Wednesday's close of $31.10 puts GES' forward P/E at 17.4. That is a pricey multiple for a company who is headed for its second consecutive year of declining revenues, and facing a two-year EPS drop of over 40 percent. Comparatively, Gap Inc. (GPS), who is expanding margins and earnings, and posting same-store sales increases, is trading at 15.7x the midpoint of its fiscal 2014 guidance. Even after backing out both company's net cash, the multiples are almost identical: 15.34 for GES, 15.42 for GPS.

By any measure, it's clear which stock investors would rather have, given the similar earnings multiples -- and it's not Guess? Guess? is now! a turnar! ound play, but its current valuation seems to have already priced in much of a potential rebound. The bull case at $31 seems difficult to make.

Of course, I argued the same thing in March at $25; what has changed is that the short case has become more compelling. In the bull market of the last few years, struggling retailers have shown surprising resilience or, at the least, the capacity to put together some quick bull moves that have damaged short sellers. Witness Sears Holdings (SHLD), Abercrombie & Fitch (ANF), and even much-maligned JC Penney (JCP), to name just a few. But GES' move near a 52-week high, and the lack of a near-term catalyst to move it beyond its recent range, removes much of the short-side risk.

Indeed, a look at the company's two-year chart, and its more recent daily chart, show a stock that appears set to turn downward:

(click to enlarge)

GES data by YCharts

Note the downtrend channel in the longer-term chart; in the second, 3-month chart, GES filled the gap after its drop following Q4 earnings in March, and may again fill the gap up following last week's release.

All told, Guess? seems to have outrun its fundamentals. Even considering its long history, its brand recognition (particularly in Europe), and its potential for a turnaround, its valuation is on par with retailers who are already succeeding, not those trying to right the ship. With some technical evidence that the near-term bull run might be coming to an end, a short sale of Guess? looks like a strong potential play.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. (More...)

No comments:

Post a Comment