As of November 2013, Ross Stores (ROST) operated 1,285 off-price retail stores offering various apparel, accessories, footwear, and home furnishings items under the names Ross and dd's DISCOUNTS. Both of these chains primarily target 25 to 54 year-old value-conscious men and women in middle to moderate income households. Ross stores, the company's primary name, average 29,300 square feet of selling space and are located in 33 states, as well as the District of Columbia and Guam. dd's DISCOUNTS store average 23,800 square feet in 10 states. Almost all of the stores currently occupy leased facilities and are in neighborhood shopping centers. The stores are primarily located in heavily populated urban and suburban areas.

Ross Stores believes that it maintains a large competitive advantage by offering a varied assortment of quality brand name and fashion merchandise, with prices 20% to 60% lower than most department and specialty stores, all while being in an easy-to-shop environment. The vendors that company deals with are never ending. Ross Stores currently deals with more than 7,900 vendors and manufacturers. They are able to offer their extremely low prices by taking advantage of supply and demand imbalances, and making their purchases later in the buying cycle than most major retailers. Many purchases of cancellations and overruns are purchased, providing perfect opportunity. The majority of orders exclude promotional and markdown allowances, as well as return privileges. Again, more reasons as to why buyers are able to obtain significant discounts on the current-season purchases.

Financial Concepts

Ross increases sales by opening new stores and retail concepts, as well as same-store sales increases. Comps increased 6% in fiscal year 2013, and 5% in fiscal year 2012. Store sales were broken down as follows: children's 8%, shoes 13%, accessories, lingerie, fine jewelry and fragrances 13%, men's 13%, home, bed, and bath 24%, and ladies' 29%.

A large proponent to margins has been the opportunistic purchasing of end-of-season items that are being held for sale the following year. The company believes that these purchases are an effective way to increase the amount of national brands in its assortments.

The company has massive potential for growth, currently only being in 33 states. During fiscal year 2013, Ross opened 62 new stores, including the entrance into three new states: Kansas, Kentucky, and Indiana. The company also opened 20 new dd's stores. Ross believes that its long-term store potential is 2,500 locations in the U.S.

Ross has more current assets than they do total liabilities. Total assets rest at roughly $4 billion with total liabilities at $2 billion. The company's dividend yield is close to a 3-year high and the P/B ratio is close to a 2-year low. The company's operating margin is expanding over time, and the per share revenue indicates consistent growth for the company.

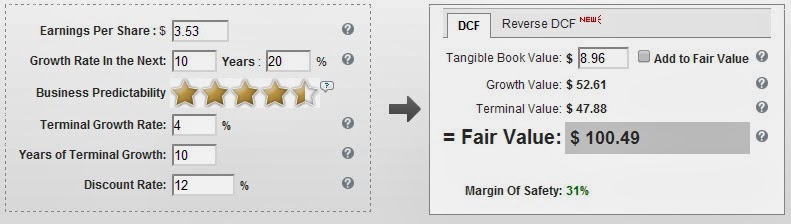

Valuation

Utilizing GuruFocus.com's DCF Calculator tool, we are able to see a fair value for Ross Stores of $100.49. This gives us a margin of safety of 31%, right where we want to be. This calculation uses an estimated 20% growth rate over the next 10 years, with a terminal growth rate of 4% and a discount rate of 12%.

According to Peter Lynch's calculation of fair value (PEG * 5-Year EBITDA Growth Rate * Earnings per Share), the company is currently worth $98.10 per share. This also gives us a comfortable margin of safety.

End Notes

Disclosure: No current position held at the time of writing.

Disclaimer: The opinions and ideas in this article are for informational and educational purposes only. They are not a recommendation to buy or sell any stock at any given time. As always, it is imperative for each individual investor to do their own due diligence and perform their own research on any and all stocks before making an investment decision.

About the author:David KerrPreviously licensed to sell securities, David now utilizes his knowledge and experience solely for the purpose of growing his own personal portfolio and educating those around him.

| Currently 5.00/512345 Rating: 5.0/5 (2 votes) |

Subscribe via Email

Subscribe RSS Comments Please leave your comment:

More GuruFocus Links

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

RSS Feed  | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

MORE GURUFOCUS LINKS

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

| RSS Feed | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

ROST STOCK PRICE CHART

69.36 (1y: +14%) $(function() { var seriesOptions = [], yAxisOptions = [], name = 'ROST', display = ''; Highcharts.setOptions({ global: { useUTC: true } }); var d = new Date(); $current_day = d.getDay(); if ($current_day == 5 || $current_day == 0 || $current_day == 6){ day = 4; } else{ day = 7; } seriesOptions[0] = { id : name, animation:false, color: '#4572A7', lineWidth: 1, name : name.toUpperCase() + ' stock price', threshold : null, data : [[1360562400000,60.86],[1360648800000,60.66],[1360735200000,60.44],[1360821600000,60.38],[1360908000000,59.91],[1361253600000,59.93],[1361340000000,58.7],[1361426400000,57.74],[1361512800000,58.16],[1361772000000,56.56],[1361858400000,56.23],[1361944800000,57.56],[1362031200000,58],[1362117600000,58.13],[1362376800000,58.9],[1362463200000,59.36],[1362549600000,59.7],[1362636000000,55.23],[1362722400000,56.2],[1362978000000,56.18],[1363064400000,55.9],[1363150800000,55.29],[1363237200000,55.87],[1363323600000,56.28],[1363582800000,56.04],[1363669200000,55.46],[1363755600000,56.17],[1363842000000,58.06],[1363928400000,59.21],[1364187600000,59.04],[1364274000000,59.43],[1364360400000,60.05],[1364446800000,60.62],[1364792400000,59.83],[1364878800000,59.41],[1364965200000,59.26],[1365051600000,60.08],[1365138000000,59.32],[1365397200000,59.32],[1365483600000,59.61],[1365570000000,60.235],[1365656400000,63.8],[1365742800000,64.67],[1366002000000,63.07],[1366088400000,63.8],[1366174800000,62.99],[1366261200000,62.51],[1366347600000,62.86],[1366606800000,63],[1366693200000,63.7],[1366779600000,63.62],[1366866000000,65.03],[1366952400000,65.12],[1367211600000,65.72],[1367298000000,66.07],[1367384400000,64.99],[1367470800000,64.66],[1367557200000,65.704],[1367816400000,65.2],[1367902800000,66.5],[1367989200000,66.13],[1368075600000,65.73],[1368162000000,65.85],[1368421200000,64.95],[1368507600000,65.73],[1368594000000,66.21],[1368680400000,64.88],[1368766800000,65.59],[1369026000000,65.12],[1369112400000,66.17],[1369198800000,65.2],[1369285200000,65.08],[1369371600000,65.84],[1369717200000,66.23],[1369803600000,65.13],[1369890000000,64.67],[1369976400000,64.318],[1370235600000,64.81],[1370322000000,64.65],[1370408400000,63.95],[1370494800000,63.66],[1370581200000,64.87],[1370840400000,64.78],[1370926800000,63.84],[1371013200000,63.53],[1371099600000,65.34],[1371186000000,64.86],[1371445200000,64.54],[1371531600000,65.31],[1371618000000,64.24],[1371704400000,63.4],[1371790800000,63.8],[1372050000000,63.29],[137! 2136400000,63.83],[1372222800000,63.72],[1372309200000,64.8],[1372395600000,64.81],[1372654800000,65.4],[1372741200000,65.45],[1372827600000,65.39],[1373000400000,66.12],[1373259600000,66.5],[1373346000000,66.45],[1373432400000,67],[1373518800000,67.24],[1373605200000,67.05],[1373864400000,66.68],[1373950800000,66.22],[1374037200000,66.06],[1374123600000,66.57],[1374210000000,66.79],[1374469200000,67.49],[1374555600000,67.05],[1374642000000,66.63],[1374728400000,67.17],[1374814800000,67.14],[1375074000000,67.09],[1375160400000,67.18],[1375246800000,67.49],[1375333200000,69.2],[1375419600000,68.93],[1375678800000,68.81],[1375765200000,67.75],[1375851600000,66.88],[1375938000000,67.13],[1376024400000,67.01],[1376283600000,67.72],[1376370000000,67.85],[1376456400000,66.64],[1376