Over the past few years, government bonds have produced almost zero income for investors. This has led to many people searching high and low for income opportunities. High-yield bonds (though recently falling out of favor) and dividend factories have benefited greatly from this search. MLPs fall into this category, as distribution yields have grown. One such MLP, EV Energy Partners (EVEP), is currently yielding over 8%, which is why it landed high on the list of stock screens. After careful analysis, it is easy to realize there is more to this company than a great yield can tell us.

When looking for an investment that will produce income, one of the major factors in the decision is the historical trend of the distribution. Is the payout ratio stable or is there risk? Does the distribution grow over time or does it stay flat?

click to enlarge images

Source: here

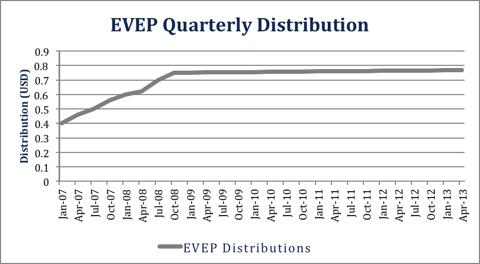

Over the past 5 years, EVEP has increased LP distributions at a constant rate of $0.016 a year or .52%. While this growth rate is anemic at best, its predictability allows us to gain insight into the actual present value of this stock.

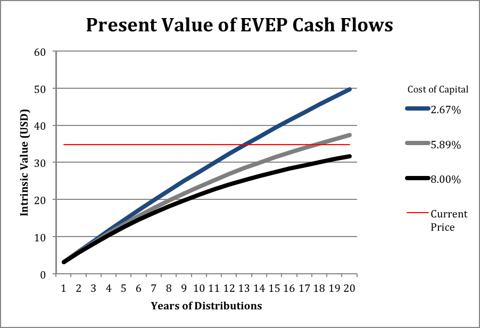

We can apply a Discounted Cash Flow (DCF) model to try to establish the intrinsic value of the position. While this model is powerful, it is entirely driven by assumptions, which can be wrong, sometimes by a great deal. Knowing (we are assuming certainty that this rate will continue) the future cash distributions of EVEP allows us to reach a target price for the stock. At a cost of capital of 5.9% and 20 years of distributions, we come to a target price of $38.

Cost of Capital Calculation | |

Risk Free Rate | 2.67% |

20 Year S&P Return | 6.70% |

Beta | 0.8 |

Cost of Capital | 5.89% |

This represents a 9% premium over the current market price, which isn't bad for an assumed risk-less investment. (We will cover large flaws in this assumption later.) At other costs of capital and distribution timeframes, we see different results.

As enticing as a 9% return is (which in this market would be underperforming by a great deal), we do not believe this to be the real potential of the stock. Our assumptions were very basic when deriving the target price of $38. There is much more to consider when analyzing a security, even one that has historically produced predictable cash flows.

Firstly, as government yields come back from their near-zero levels, the cost of capital will increase along with it. The opportunity cost of capital invested in this MLP will increase greatly as the risk-free rate comes up. As the cost of capital increases, the present value of future cash flows drops substantially. At only an 8% cost of capital, the NPV of EVEP distributions drops below the current market price, which means to keep up, the growth rate of distributions would need to increase greatly.

Secondly, we made the assumption that the distributions will continue for another 20 years. The average lifespan of an S&P 500 company is approximately 15 years (BBC.co.uk). EVEP began in 2006, which makes it 7 years old. If it lasts as long as the average S&P company, it means there are only 8 years of distributions left, which translates to a DCF of $20 or a 43% discount to today's price. If it lasts 15 years from today, the NPV of the distributions is only $31 or an 11% discount. For it to last 20 years from today it will have to almost double the average S&P company.

Finally, we must consider whether EVEP can continue a dividend at all. To maintain its current growth rate, EVEP would need to grow its cash reserves immediately. In 201! 2 and the! first part of 2013, EVEP has financed its distributions through issuance of stock and debt. While this has allowed them to maintain their distribution stability, they are becoming more financially unstable. In order to start unwinding debt while maintaining distributions, EVEP will have to grow its cash organically through operations. Net income has decreased over the past three years, even as revenues have increased. This is largely due to management's inability to contain operating expenses, which may be a sign that EVEP will have to restructure soon, which could destabilize the distributions.

EV Energy Partners' predictability and high yield make for a cautiously interesting investment opportunity. We do not believe now is the time to invest; however, we are looking for signs of a turnaround in the next year or so. Potential acquisition agreements and an already decent balance sheet could make it easier for an EVEP turnaround than other MLPs in the same position. While I will not be initiating a position in the near future, this high yielding investment is one to watch closely for some positive changes.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. (More...)

No comments:

Post a Comment