I'm going to attempt something a little odd today, Fools. Even though IPG Photonics (NASDAQ: IPGP ) -- a company that makes fiber optic lasers -- makes up 5% of my real-life holdings, I'm going to be giving you two reasons to consider selling IPG stock today.

Why am I doing this?

Recently, Nobel Prize winner Daniel Kahneman visited Fool headquarters in Virginia. While visiting, he talked about how a number of different biases can lead us to believe we can predict the future with relative certainty. In reality, he argued, we're just deluding ourselves.

It got me to thinking about how I don't write enough about the risks of owning the stocks I own. So although I don't plan on selling my IPG stock anytime soon, I think it's healthy for me to practice and model this behavior.

Let's go over the three points.

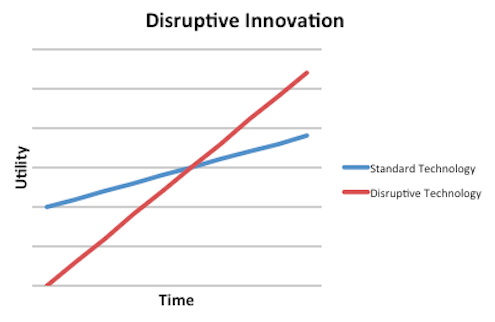

Disrupting the disruptor

When I purchased shares of IPG Photonics last April, I used this chart as the basis for my investing thesis.

Source: Author, based on The Innovator's Dilemma by Clayton Christensen

This is my own representation of an idea gleaned from Clayton Christensen's The Innovator's Dilemma. The book demonstrates how new technologies eventually usurp standard technologies. Just as important, while standard technologies usually maintain the same price point, newer technologies become cheaper with time.

For decades, the standard technology in the laser industry has been the carbon-based laser. In reality, these lasers are still commonly used, and sold in bulk by the likes of Rofin-Sinar (NASDAQ: RSTI ) and Coherent (NASDAQ: COHR ) . They are used largely for precision cutting of large pieces of metal.

But starting in the 1990s, when IPG was founded, a new type of laser began developing. Though IPG's fiber optic lasers were at first far too expensive, and not powerful enough, to gain wide acceptance, that has changed with time. Now, IPG's lasers are more efficient, and powerful, than their carbon-based partners, and can compete on price to boot!

The problem, however, is that there could be further disruption right around the corner. I am far from being an expert in lasers -- and I'm guessing the same is true of many Fools. Because of that, it's going to be very difficult for me to see a newer laser -- one that's even cheaper and more powerful than fiber optics -- coming to the market. If that does happen, IPG could quickly lose market share.

The downside of vertical integration

While IPG was the first on the scene with fiber optic lasers, it's no longer the only company with skin in the game. Rofin-Sinar and Coherent now offer fiber optic lasers along side their carbon lasers. Furthermore, JDS Uniphase (NASDAQ: JDSU ) , which focuses much more on the communications industry, has entered the fray by offering clients fiber optic lasers.

With the competition, IPG decided to further differentiate itself by becoming vertically integrated. Usually, a laser-making company will contract out for component parts, like laser diodes, to be delivered and then assembled by its own people. IPG, on the other hand, does everything—from manufacturing the small component parts to assembling them to shipping them off the customers—in house.

During boom times, this is great for business. IPG is able to get all of its component parts for much cheaper than JDS, Coherent, and Rofin-Sinar. That makes it easier to turn a profit and/or offer lasers for cheaper than the competition.

During difficult economic times, however, the situation gets flipped on its head. JDS, Rofin-Sinar, and Coherent can simply order less component parts and spend less money in the face of less demand. IPG, however, has a certain amount of fixed overhead costs it will have to pay no matter the economic climate.

IPG stock, therefore, can get hit much harder during downturns than the competition's.

What's a Fool to do?

To be honest, the concerns over vertical integration don't bother me too much, as I think the boom times typically occur with greater frequency than bust times. The first concern -- over being disrupted -- is one that I definitely need to keep my eye on.

Another disruptive innovator that I own and believe in is growing twice as fast as Google and Facebook, and more than three times as fast as Amazon.com and Apple. Watch our jaw-dropping investor alert video today to find out why The Motley Fool's chief technology officer is putting $117,238 of his own money on the table. Find out why he and I are so confident this will be a huge winner in 2013 and beyond. Just click here to watch!

No comments:

Post a Comment